TSB, one of the UK's largest retail banks, spent several years planning a migration off a legacy banking platform. When the switchover went live, a significant proportion of its 5.2 million customers were locked out of their accounts. And some were given access to the confidential records of others. The bank paid £32 million in customer redress, was fined £48 million by regulators, and lost around 80,000 customers that year. The total cost exceeded £300 million.

Stories like this don't inspire confidence about legacy modernization in fintech. And that helps explain why so many European financial institutions remain dependent on software built 10 to 20 years ago. The systems may be old, but they continue to process payments and support critical business operations every day. Replacing them carries risks that most financial leaders aren't willing to take without a clear reason to act.

But standing still also creates problems, since sooner or later, systems that work become difficult to extend. There is no universal answer to what comes next. Sometimes building around the existing core is the right call. Sometimes the core itself has to go. And sometimes the legacy isn't the software at all. Below, we examine four real-world fintech projects and the reasoning behind each modernization decision.

Most financial institutions know their systems need to change. The first decision, where to start, usually determines whether the project succeeds or fails. Choose the wrong entry point, and you can break what still works.

For example, if the core system still processes transactions reliably, the right move is to build around it, like add a customer-facing layer or introduce new services on top. If the core itself has become the ceiling, working around it only delays the inevitable. At some point, it has to be replaced.

Over the last 13 years in fintech, we've come through different scenarios. The four cases below cover legacy modernizations in payments, wealth management, insurance, and accounting. Each one produced a different answer to the question: what can we build on, and what has to go?

TWINT is Switzerland's national payment app, serving more than 6 million users. To strengthen its position against global wallets such as Apple Pay and PayPal, TWINT had to expand beyond payments. They partnered with Modeso to build new user-facing and partner-focused modules, including Digital Voucher, Super Deals, Storefinder, InsurHub, and Spin & Win.

A system serving millions of users cannot be paused for upgrades or tested in isolation from real-world traffic. Every new module had to work within the current architecture, comply with Swiss financial security requirements, and maintain performance under load. The transaction-processing core was solid, so we built and scaled new capabilities around it.

Our partnership has been running since 2020. During that time, TWINT evolved from a payment application into a broader digital marketplace and ecosystem. Digital Voucher grew into a marketplace that has sold over 3 million vouchers, while Super Deals supported roughly 300,000 redemptions. Engagement features such as Spin & Win generated nearly 6 million user interactions.

Our takeaway → TWINT's transaction infrastructure already worked at scale. We built around that foundation and expanded what the platform could do without putting day-to-day operations at risk.

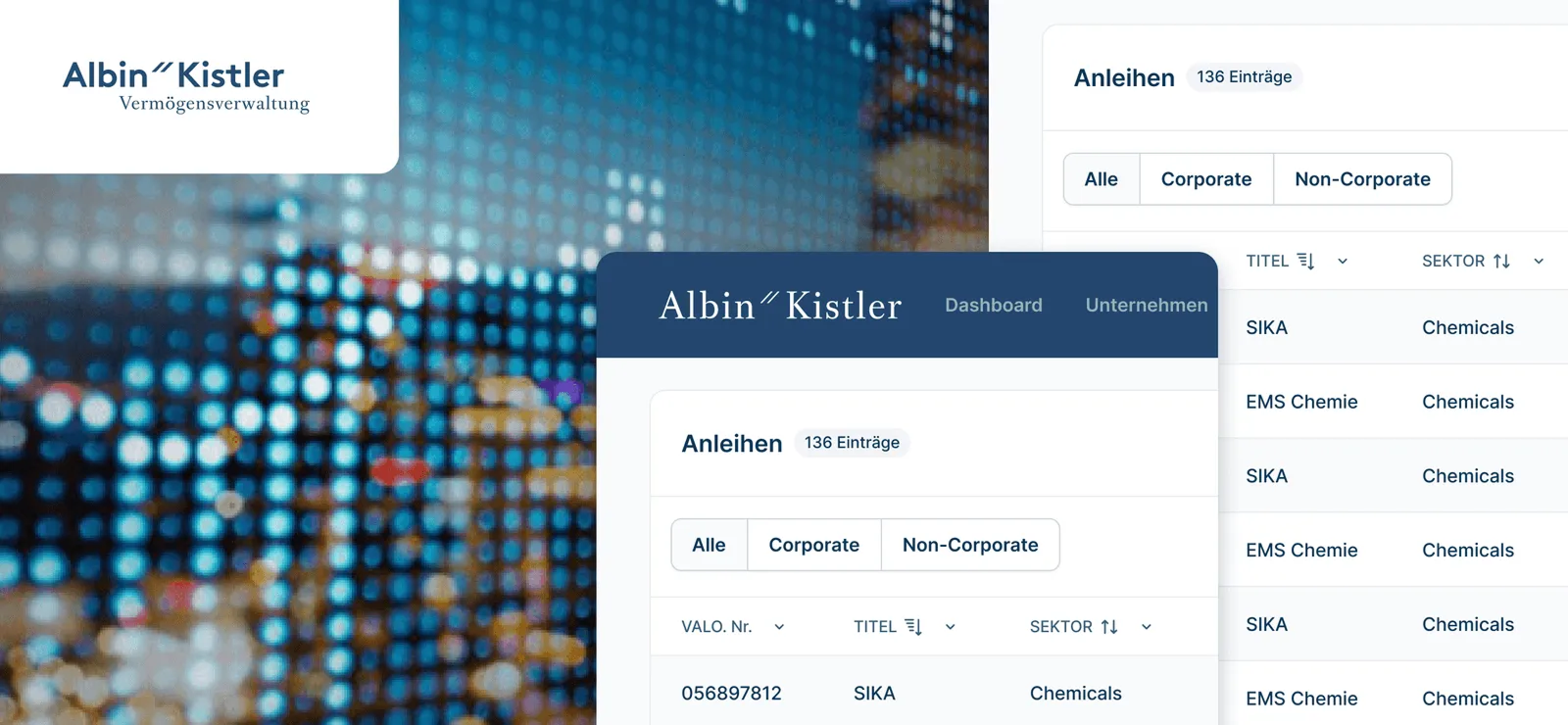

Albin Kistler manages more than CHF 6 billion for private and institutional investors across Switzerland. The firm's investment decisions are supported by a proprietary algorithm that captures 25 years of investment expertise. For years, that system ran on Microsoft Access and delivered reliable results. As the system evolved, its logic grew harder to maintain. The algorithm remained trusted, but every change carried risk because much of the underlying logic was not fully traced.

When we joined the project, we had to understand the existing system first. The team spent weeks reverse-engineering the application, documenting calculations, dependencies, and data flows until we could map the complete logic from data input to final output.

From that point, it was clear that building on top of the existing platform wasn’t viable. We rebuilt the system from scratch, starting with the calculation engine. Once the foundation was validated, development expanded to the user interface, integrations, and additional capabilities. The new platform integrated with SIX apiD for market data, Expersoft PM1 for customer and portfolio information, and Albin Kistler's Active Directory for authentication. Deploying new features now produces 90% fewer bugs, and release cycles move 50% faster.

Our takeaway → Sometimes the right modernization entry point is a complete rebuild. But rewriting the code is the easier half. The biggest risk is losing track of how the old system worked. We managed that risk through phased delivery, continuous UAT, and documented milestones at every stage. From planning to rollout, we took ownership of the process to modernize the platform without losing the logic that made it valuable in the first place.

Learn more about how we approach projects like this in our article on digital transformation in wealth management.

Würth Financial Services is one of Switzerland’s leading insurance brokers. The firm had long-standing provider relationships and a customer base built over decades. What it didn't have was a digital channel that could reach new customers at scale.

TWINT had become that channel. Six million people were already opening the app to pay for things daily. Würth saw the opportunity to connect their existing insurance products to a platform where millions of potential customers already were. TWINT liked the idea and recommended Modeso to build it, since we had already spent years working inside the platform.

That prior experience mattered. TWINT's certification process can add months to a launch timeline. Because we already understood the requirements, we could focus on building the product instead of learning the process under deadline.

In three months, we built InsurHub, a backend connecting Würth, TWINT, and multiple insurance providers into a single system. Users could browse, compare, and purchase policies without leaving the app. The in-app experience was designed to look and feel like the rest of TWINT.

InsurHub sold 15,000+ insurance policies in its first year and won second place at the 2022 Swiss Insurance Innovation Award.

Our takeaway → New digital products don’t always require new infrastructure. Würth already had the insurance products and partner network. TWINT already had the audience. The challenge was connecting them quickly and reliably. And we could do that because we already knew the platform we were building inside.

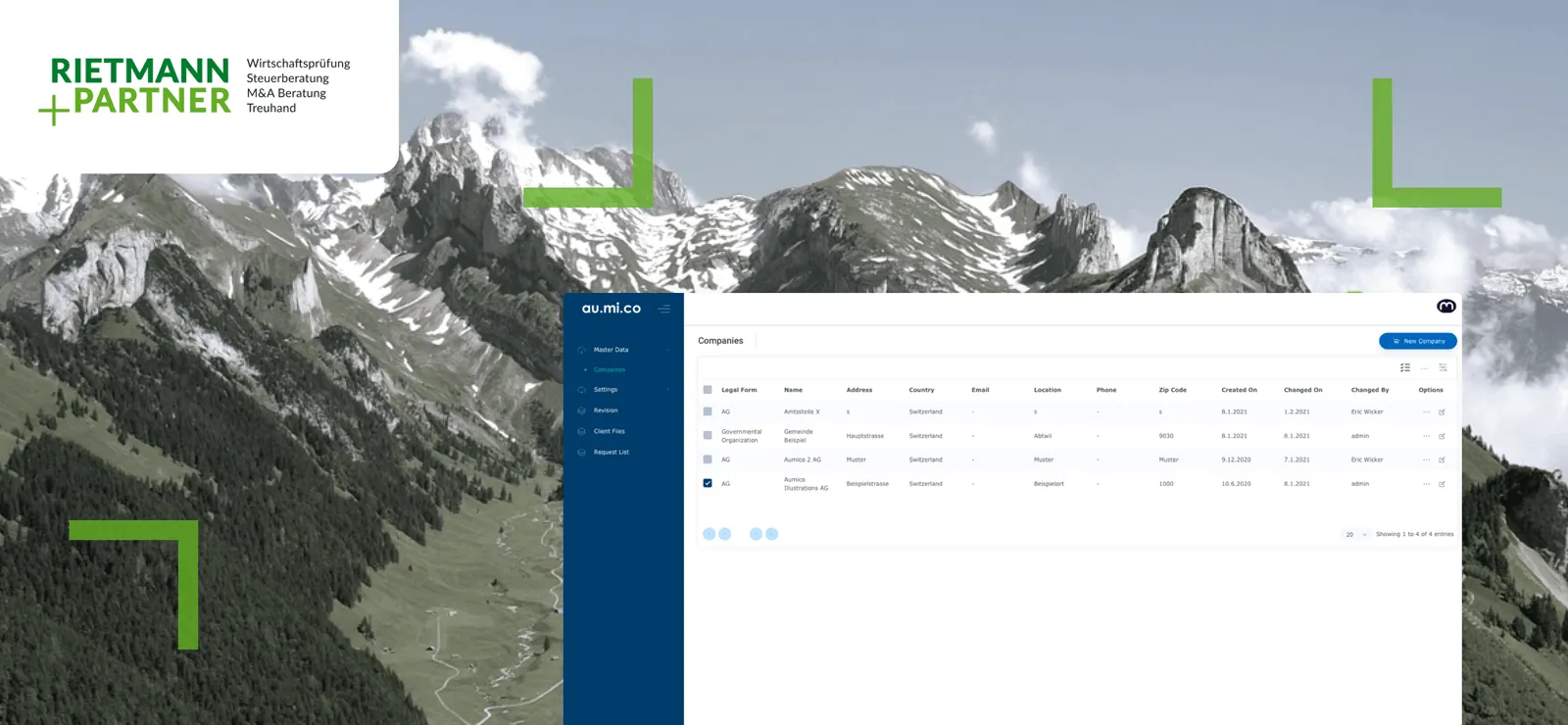

Rietmann und Partner has been conducting audits in Switzerland since 1911. Like many audit firms, its work relied on expert knowledge and manual processes. As the firm grew, that approach became harder to scale. Auditors had to navigate complex procedures manually, creating inefficiencies and increasing the risk of inconsistencies.

The firm evaluated existing audit software but found that none matched the way its teams worked. Most tools were too generic, too rigid, or designed for regulatory contexts that had nothing to do with Swiss auditing. So they came to Modeso to build it from scratch.

First, we tried to understand how auditors planned engagements, reviewed financial statements, identified risks, and documented findings. Only after mapping those workflows did development begin. We designed a configurable, rule-based platform that guides auditors through the entire process, from data import and analysis to task execution and report generation.

Rietmann & Partner gained a platform that standardized audit workflows, reduced manual effort, and created a foundation for expansion beyond Switzerland.

Our takeaway → Not every digital transformation starts with new technology. Sometimes the real asset is the expertise that already exists inside the business. We turned that expertise into a scalable software system.

Four fintech modernization patterns

In one form or another, all four examples above are stories about legacy modernization in fintech. Each organization faced a different constraint, and each required a different starting point. The same principle applies to AI initiatives.

But before you decide how to implement AI, you need to understand where it can have the greatest impact.

At Modeso, we start every AI engagement by identifying the right entry point. It’s the one process where AI can deliver a measurable improvement and prove its value quickly. We scope a pilot around a single business outcome, deliver it in weeks, and then scale what works. For that, we become your external AI department. Within 12 weeks, we deliver a production-ready AI agent for a fixed fee of CHF 15,000:

We analyze your processes, identify the highest-impact AI opportunities, and define measurable KPIs. You get a technical concept and ROI forecast.

We build the AI agent and integrate it into your existing infrastructure.

We go live, monitor performance, and optimize until the KPIs are met. We don't hand over and disappear.

If you want to keep going, we continue as your dedicated AI team. If the agreed KPIs aren't met after 12 weeks, you get a CHF 10,000 fee back. The technical concept, a blueprint valued at CHF 5,000, stays with you regardless.

This way, you can move on AI without a years-long commitment. You get a focused first step and a team that owns the outcome.

The projects above look nothing alike on the surface. Except they’re all fintech. But they all required a deep understanding of the existing system to know where to start. And enough ownership to stay accountable for what that decision produced.

In fintech, accountability matters more than in most industries. The TSB case already showed what that cost looks like – £300 million and years of recovery. Compliance, security, and performance have to be baked in by the team that's going to live with the consequences. We call it full-cycle development. The same team that identifies the constraint stays responsible for solving it, from discovery and architecture to development, testing, rollout, and ongoing improvement.

That kind of ownership pays off beyond the modernization itself. Along with fixing what’s broken, financial institutions need platforms that can support AI. Most legacy systems weren't built for it. When modernization, AI implementation, and future product development sit with the same team, the foundation and everything built on top of it are designed to work together from the start.

Since 2013, we've helped financial institutions across the DACH region modernize payment platforms, investment systems, insurance products, and operational workflows. In every case, the objective was the same: make the right change in the right place and take ownership of the outcome.

Privacy is important to us, so you have the option of disabling certain types of storage that may not be necessary for the basic functioning of the website. Blocking categories may impact your experience on the website. More information