Over half of the finance companies outsource fintech software development. Yet here’s what many founders tend to overlook: outsourcing in fintech is nothing like outsourcing a typical SaaS or mobile app.

As an outcome, many fintech outsourcing projects fail.

All because fintech development is fundamentally different. In fintech, every product must keep up with compliance requirements, financial logic, risk, and security. That means higher complexity from day one, and it’s the reason why classic outsourcing often falls short.

So founders are turning to full-cycle fintech development instead. This gives more security, compliance from the onset, and a partner who’s devoted to your project (if you’ve found the right one, of course). But full-cycle development comes with its own challenges that founders need to understand before they begin.

At Modeso, we’ve delivered 90+ fintech and finance-adjacent products for Swiss institutions, scaleups, and global players. We’ve seen where projects typically stumble and ways they overcame the pitfalls.

In this guide, we break down the full cycle from alignment to maintenance and the 7 challenges you’re likely to face at each step.

If you’re considering full-cycle fintech development or want to evaluate it against fintech outsourcing, start here.

Choosing how to build your fintech product is one of the most expensive decisions you’ll make. And each model comes with very different realities. Here’s the short comparison.

If you already have strong fintech product leadership and your project is narrow and well-scoped, outsourcing may work, but only if you invest heavily in alignment and oversight.

If you’re building a core fintech platform and want full control and ownership, go in-house, but budget for time and cost accordingly.

For most early-stage or scaling fintechs, full-cycle development offers the best balance of cost, speed, risk, and outcome.

That said, let’s review the full-cycle fintech development stage by stage to see the challenges of each one, starting with the typical issue of the alignment stage.

Once again, fintech products aren’t typical apps. They are built on top of complex payment flows, KYC/AML rules, risk logic, transaction monitoring, ledger behavior, and regulatory frameworks that change constantly.

If your team doesn’t deeply understand your business model, financial workflows, regulatory obligations, and target customers, then they will make the wrong assumptions, which will become extremely expensive to fix later.

This is one of the most common financial software challenges: a development team technically executes tasks, but doesn’t understand the financial system they're building for.

A strong full-cycle fintech development partner takes responsibility for alignment. This means:

This is what separates a dedicated fintech development team from generalist developers or outstaffed engineers.

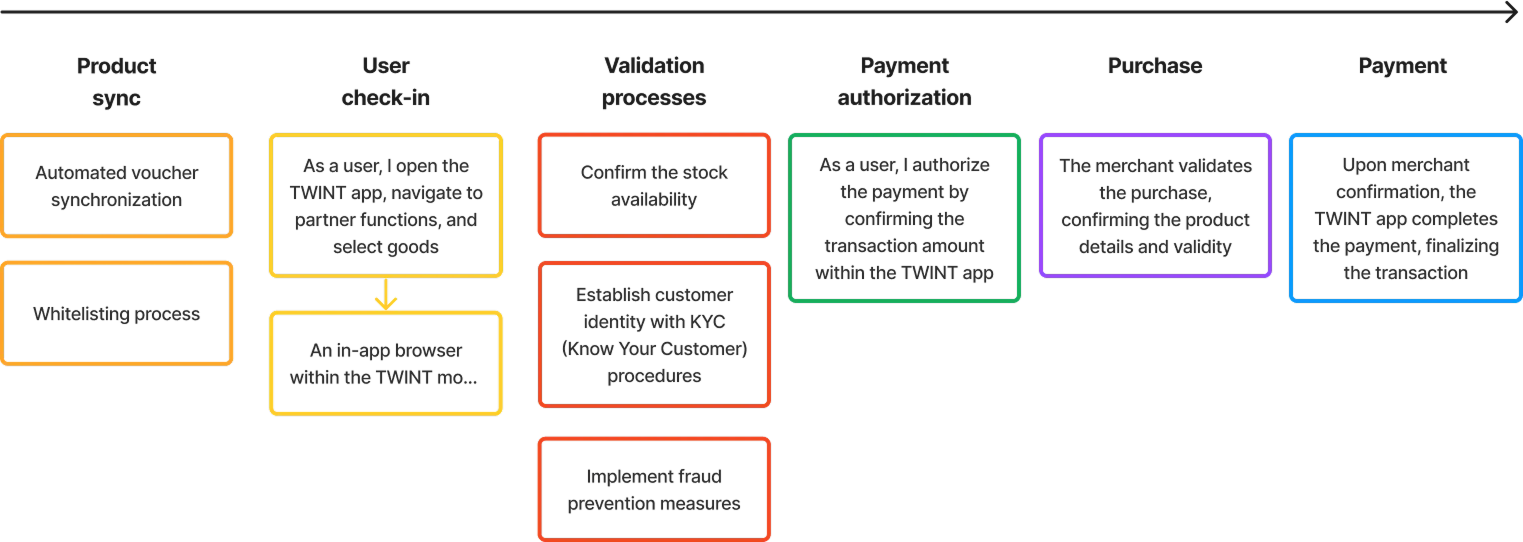

When we worked with TWINT, Switzerland’s leading mobile payment platform, we didn’t jump straight into implementation. Instead, we invested time understanding:

This alignment phase shaped the entire project. It allowed us to build a digital voucher marketplace and merchant-offer platform in a way that fully met the user's needs.

Start full-cycle development with alignment as your first priority. It paves the way for every stage that follows.

One of the biggest traps in fintech software development is assuming it will cost and behave like a basic app build. It won’t. Hidden complexity (compliance, security hardening, integrations, audits) means costs can escalate fast, especially if you treat full-cycle development like generic fintech software outsourcing.

What usually goes wrong:

Result: underestimated budget, slipping deadlines, and a roadmap that has to be rewritten halfway through.

Instead of one vague “build the product” line item, structure your fintech development project around clear stages with separate expectations and pricing:

A good fintech development partner will be transparent about pricing models in fintech development outsourcing versus full-cycle engagement, and will help you see not just what it costs per sprint, but what it costs to launch, pass audits, and operate safely in production.

In fintech, UX = compliance. Every screen, flow, and micro-interaction must respect financial regulations, data-handling rules, risk controls, and user-protection standards. A design that looks great but fails to meet KYC/AML, PSD2/FINMA, PCI-DSS, consent management, disclosure, or auditability requirements is not a design you can ship.

This is where many teams get blindsided. They design like it’s a generic SaaS product to later discover that regulators expect specific steps, explanations, data-visibility constraints, or mandatory user actions.

Treat compliance as a design constraint from day one.

At Modeso, we build interfaces with fintech experts involved at the UX stage, not after. That means:

✅Product, design, and compliance sit together when we map the user journey.

✅We decide where to ask for which data, how to explain it to users, and what to log for audits before any high-fidelity UI is created.

✅Designers work with engineers who understand how banks, PSPs, KYC providers, and regulators expect flows to behave.

This way, flows feel simple to users but already meet regulations, so you don’t have to redo half your UX right before launch.

At the development stage, a lot of full-cycle projects fail for a simple reason: the team has solid general skills (Python, React, cloud, etc.) but no real fintech expertise.

In a fintech software development project, that gap is dangerous. Mistakes here lead to rework, delays, and compliance risk.

Instead of teaching a generalist team “how finance works” on your budget, you bring in a full-cycle fintech development partner that lives and breathes fintech every day and has a portfolio of successful projects in fintech.

At Modeso, we specialize in custom fintech software development for financial services, insurance, asset management, audit/tax firms, and ambitious fintech startups. Our 10+ years of industry experience allow us to build fintech products that are:

%202.png)

When integration isn’t planned from the start, full-cycle fintech projects often hit roadblocks: data flows break, teams build workarounds, and technical debt piles up. The outcome is duplicate data, manual processes, operational inefficiencies, and scalability limits.

Here’s the process we use at Modeso and what we can recommend to any fintech development team:

In our blog about system integration, we observed that companies treating integration as an afterthought accumulate technical debt, which comes much more costly at the end.

When integration is part of your full-cycle plan, you avoid messy retrofits and deliver a fintech product that scales and integrates seamlessly with the ecosystem.

In fintech, handing off tasks to an external team without giving them full product responsibility is a major risk. You might get capable engineers, but you don’t get a team that understands the business context, the regulatory pressure, or the long-term technical decisions your product depends on.

And when something goes wrong, like a failed audit, a blocked banking integration, or a scaling incident, you suddenly realize the downside of out-staffing: no one owns the outcome.

You end up switching vendors, re-explaining the domain, managing messy hand-offs, and absorbing responsibility for defects yourself. In a highly regulated industry, that’s too dangerous. Operational risk increases, audits get harder, and continuity breaks down.

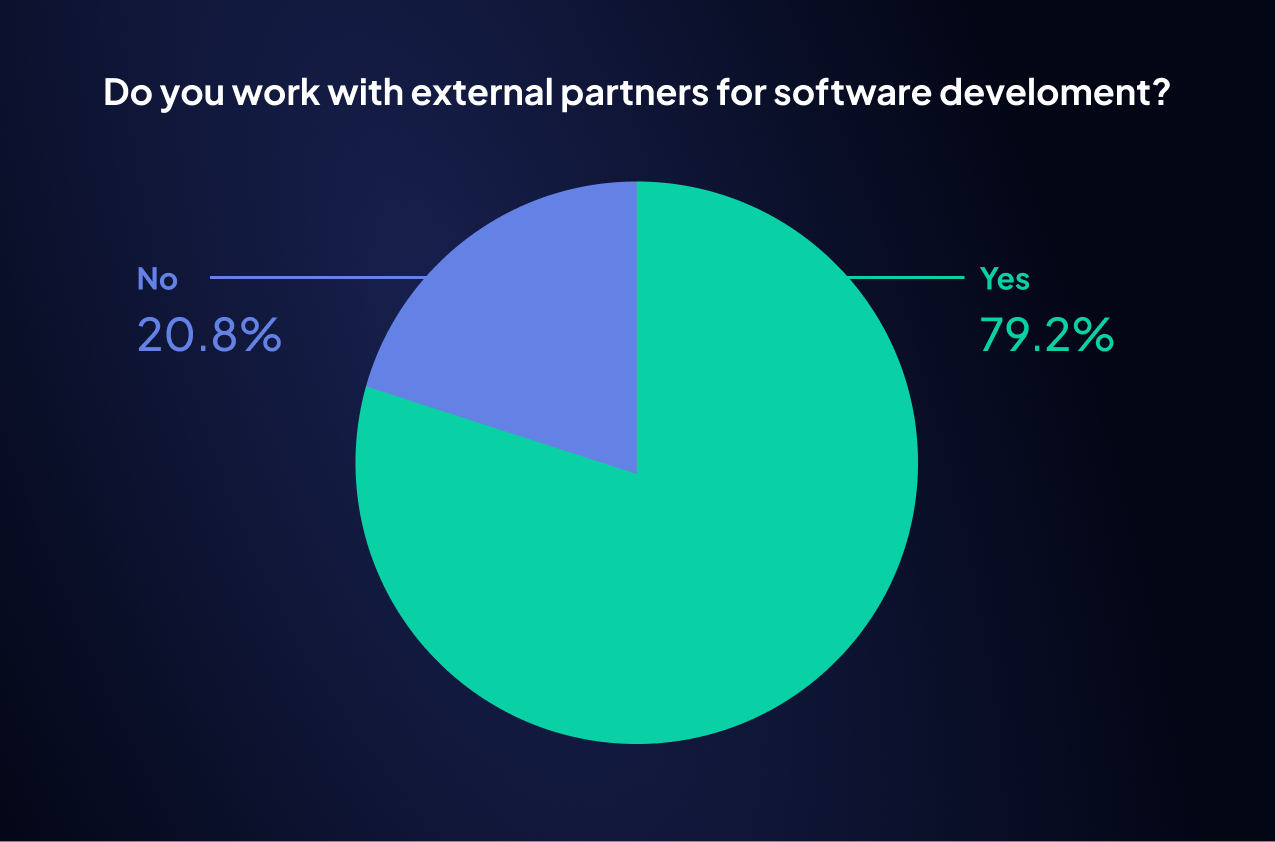

Our survey of 200 European tech leaders found that 79,2% of teams work with external partners for their development, and many choose a full-cycle team for more stability and confidence.

A full-cycle team takes responsibility end-to-end: product strategy, UX, architecture, integrations, compliance readiness, deployment, monitoring, and continuous improvement. They evolve the product after release rather than disappearing when sprints end.

This is exactly how Modeso works with fintech clients. Swiss-based product ownership combined with our experienced engineering hubs means the same team that designs your solution is the one integrating it, hardening it for audits, and supporting it in production.

Launching a fintech product isn’t the finish line. In fact, it’s the point where the real security work begins, especially regarding ever-evolving regulations. In Europe, 75% of financial compliance leaders reported a 35% increase in regulatory demands in 2024.

If you don’t maintain tight, continuous security practices after release, you risk:

In fintech, “set it and forget it” simply doesn’t exist.

A full-cycle development partner understands that release is only Phase 1. Security, compliance, and operational hygiene must continue as part of the product’s lifecycle.

At Modeso, we stay with our clients after launch because regulated products need ongoing care. We continue to:

This long-term vigilance is one of the core strengths of full-cycle development, and one of the biggest weaknesses of one-off outsourcing or outstaffing.

Full-cycle development isn’t a silver bullet. You’ll still face hard choices about scope, costs, integrations, compliance, security, and long-term ownership.

The difference is that with full-cycle, you’re not fighting those battles alone or in the wrong order.

If you remember anything from this guide, let it be this:

We’ve used these lessons across 90+ fintech and finance products. If you’re planning to build a fintech product, we’ll be glad to help you overcome every challenge. Contact us, and we’ll get back to you in 1-2 business days.

But even if you don’t build with us, use this guide as your checklist. It will save you time, money, and a lot of “we should’ve known this earlier” moments.

Privacy is important to us, so you have the option of disabling certain types of storage that may not be necessary for the basic functioning of the website. Blocking categories may impact your experience on the website. More information